With growth moderation likely in the second half of the year for exports, agriculture, and construction—and with continued contraction in mining—GDP growth for the whole year is now seen slightly lower than earlier forecast. As inflation is on an upward trend and unlikely to change course in the near term, inflation forecasts for this year and next are revised up. The current account surplus is forecast to narrow more than foreseen in April.

Photo: tapchitaichinh.vn

Updated assessment

Vietnam posted 7.1% GDP growth in the first half of 2018, up from 5.8% in the same period in 2017. On the demand side, rising income lifted private consumption growth to 7.2% from 7.0% a year earlier. Private investment remained robust, supported by high credit growth and strong foreign direct investment (FDI).

Exports of goods and services rose by 15.7% by volume in the first half of the year from 14.4% a year earlier. Strength in exports, domestic private consumption, and investment more than offset deceleration in government consumption and public investment that resulted from fiscal consolidation.

Most major sectors continued to perform solidly. Output from agriculture and allied activities grew by 3.9% in the first half of this year, up from 2.7% in the first half of 2017. Thanks to favorable weather and strong export demand, farm output increased by 3.3%, up from 2.1% growth in the first half of 2017, while forestry and fisheries also remained buoyant.

Industrial production expanded by 9.3% in first half of the year, sharply higher than 5.4% expansion in the same months of last year. A 13.0% rise in manufacturing output was driven by impressive increases in export-oriented sectors such as in telecommunications, electronics, and textiles.

Acceleration in industry more than offset moderation in construction from 8.5% growth in the first half of last year to 7.9% this year as measures took hold to curb bank lending to real estate. Driven partly by a hefty rise in international tourist arrivals, the service sector posted nearly 7.0% growth in the first half of the year, the same pace as in the first 6 months of last year.

As tourist arrivals rose by 27.2% in the first half, hotels and restaurants, transportation and communications, and wholesale and retail trade continued to be buoyant.

Strong growth put upward pressure on inflation, as did a hike in government-administered fees and higher international oil prices. Headline inflation inched up to 4.7% year on year by June 2018 from the low of 2.5% in June 2017, and average annual inflation in the first 6 months of the year reached 3.3%.

Driven by hikes in several administered fees, prices for medical services surged by 16.7% in the first half of the year while tuition for public education increased by 6.8%. Meanwhile, transportation costs went up by 9.7%, largely because of higher gasoline prices.

The balance of payments posted an estimated surplus equal to 8.4% of GDP in the first half of the year, with the current and capital accounts both registering surpluses. Helped by a merchandise trade surplus in the first half, the current account yielded a surplus estimated to equal 5.0% of GDP, reversing a deficit of 1.1% in the same period a year earlier.

The trade surplus was made possible by 17.0% growth in merchandise exports that far outstripped 10.5% growth in imports. The main items experiencing export growth were mobile phones and other electronic products, which now account for 31.6% of all exports, up from 11.5% in 2011.

Bolstered by strong FDI and rising portfolio capital inflows, the capital account recorded a surplus equal to an estimated 7.9% of GDP in the first half of 2018. FDI commitments reached USD16.2 billion in the first six months, and disbursements an estimated USD8.4 billion, up by 8.4% year on year. A major part of FDI flowed into export-oriented manufacturing of mobile phones and other electronics.

Meanwhile, net portfolio capital inflows came in at an estimated USD2.3 billion in the first half of the year further helping the capital account to post a surplus. Official foreign exchange reserves thus rose from an equivalent of 2.7 months of imports at the end of 2017 to an equivalent of 3 months import cover by June this year. Meanwhile, the Viet Nam dong, having remained stable against the US dollar in the first 6 months of the year, depreciated by about 1% in June, partly in response to rising US interest rates.

The stock market was volatile in the first half of the year, rising to an 11-year high of 1,200 at the beginning of April, slumping below 1,000 in May-July as interest rates and returns on capital rose in other capital markets, and then gradually recovering.

Despite upwardly creeping inflation, State Bank of Viet Nam (SBV), the central bank, maintained its policy interest rates unchanged since a cut in July 2017, in an attempt to keep monetary and credit growth in line with its official targets.

At the end of June 2018, growth in the money supply (M2) was an estimated 16.2% year on year, and growth of bank credit was 15.0%, largely in line with the SBV’s annual targets.

The government’s fiscal consolidation program progressed in the first half of the year. Budget revenue increased by 15.7% in the first 6 months, reaching the equivalent of 28.7% of GDP.

Meanwhile, expenditure increased by a more modest 11.4%, thanks partly to the rationalization of spending, though still slower than originally planned. The budget posted a small surplus equal to 0.1% of GDP in the fi rst half of the year, reversing a defi cit of nearly 1.0% a year earlier. Eff orts to rein in the fi scal defi cit helped to lower the ratio of public debt to GDP to an estimated 58.5% at the end of June 2018 from 63.7% at the beginning of 2017.

Structural reform of state-owned enterprises (SOEs) and the banking system continued in the fi rst half of 2018, though at a lackluster pace for the former. Although selling of government stakes in 16 SOEs and divestment of state capital added about D28 trillion to the budget, it was only one-fifth of last year’s fi gure. Meanwhile, equitization plans were approved for only 19 SOEs in the fi rst half of the year, way behind the government’s target of equitizing at least 85 SOEs before year-end.

The share of nonperforming loans (NPLs) in the banking system fell to 2.1% in June 2018, down from 2.5% at the beginning of 2017 as banks stepped up NPL resolution through debt collection and the sale of collateral. Meanwhile, all NPLs on bank balance sheets and warehoused with the state-owned Viet Nam Asset Management Company, combined with bank loans deemed at high risk of becoming NPLs in the near term, were estimated by the government at 6.9% of all outstanding loans in mid-2018, down from the 10.1% in December 2016. NPL resolution has received fresh impetus from the legal reform eff ected in 2017 that facilitated the disposal of collateral and the restructuring of bad assets.

Prospects

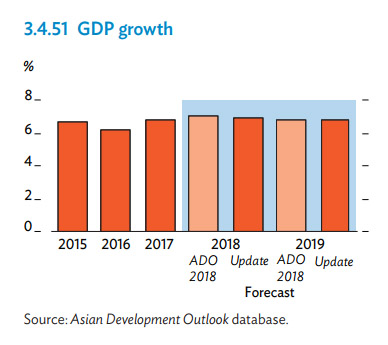

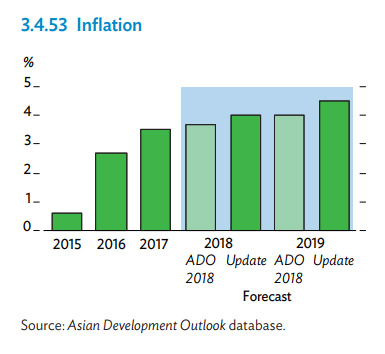

Economic growth will likely hold up fairly well in the near term thanks to continued strength in domestic demand. However, growth moderation in the European Union, Japan, and the People’s Republic of China could dent export opportunities for Viet Nam, as could escalating trade friction around the world that threatens to disrupt global value chains and production networks in which Viet Nam is tightly integrated. Severe fl oods in July and August could undermine agriculture, while aging mines will likely drive down mining output. The growth forecast for this year is therefore revised down from 7.1% in ADO 2018 to 6.9%, while the forecast for 2019 is retained. Meanwhile, inflation forecasts are adjusted upward from 3.7% to 4.0% for 2018 and from 4.0% to 4.5% for 2019.

Prospects for private consumption continue to be bright, while the outlook for private investment remains stable under the government’s continuing eff orts to improve the business environment and facilitate the opening of new businesses. Acceleration in public capital expenditure in the second half of the year is expected to boost growth in investment.

Growth in merchandise exports is likely to moderate in the near term although Viet Nam’s participation in various free trade agreements should support continued access to foreign markets for major exports.

By sector, agriculture should post slower growth at 2.5% this year, below the earlier forecast and the government target of 3.0%, following severe fl oods in recent months. Mining output, which contracted by 1.3% in the fi rst half of the year, continues to be handicapped by aging mines, oil fi elds, and unfavorable weather conditions. Growth in construction will moderate in the rest of the year as the government seeks to prevent a real estate bubble. The manufacturing purchasing managers’ index reached a record high of 55.7 in June, indicating continued improvement in business conditions, but some softening in industry growth cannot be ruled out as exports moderate in the coming months.

Meanwhile, services are likely to hold up well thanks to rising private consumption and buoyant tourism. Despite the downward revision for growth this year, infl ationary pressures are likely to persist over the near term.

The dong has exhibited more weakness since July and could come under continued pressure as US interest rates rise and the dollar strengthens. Depreciation of the renminbi against dollar, if it continues, could further put pressure on the dong, adding to infl ation. Moreover, the rise in international oil prices will raise the pressure on infl ation, as would an upsurge in food prices. Food prices, with a weight of around a third in the consumer price index, have already risen by 2.3% in the fi rst eight months of the year, reversing their declining trend in the same period last year. Average annual infl ation is therefore forecast to edge up to 4.0% in 2018 and further to 4.5% in 2019, both projections higher than in April.

The emergence of trade defi cit in July and August signaled that growth in merchandise imports is likely to outpace that of exports. The current account surplus will likely narrow even if net service exports remain steady. Forecasts for the current account surplus are therefore revised down to the equivalent of 2.3% of GDP this year and maintained at 2.0% next year. On the capital account, FDI continues to be a major source of strength. However, if trade tensions escalate, foreign investors may consider adjusting their business strategies, dampening FDI infl ows to Viet Nam. Although FDI remained strong in the fi rst half of this year, it has been less buoyant since then.

Amid the complexities of the emerging macroeconomic environment, Viet Nam is cautiously deploying fi scal and monetary policies to maintain stability while supporting growth. Fiscal policy continues to focus on broadening the tax base and strengthening tax administration. Although the central bank has kept its policy interest rate unchanged, it has taken other measures to stabilize the exchange rate, notably selling USD to commercial banks in July and August.

Interest rates for central bank bills issued since late July have also been adjusted upward, pushing up the interbank money market interest rate. Going forward, the SBV intends to pursue a more flexible exchange rate regime with the ultimate objective of gradually shifting its monetary policy framework from focusing on exchange rate stabilization and monetary-credit targeting to inflation targeting. Building on these recent measures and future policy intentions, there is merit in a tighter monetary policy in the near term to rein in inflation.

Risks to the outlook are mostly on the downside. If escalating trade tensions around the world slow global trade substantially and disrupt global production networks and supply chains, the growth outlook for Viet Nam will be much dimmer. Not only would such developments hurt its export prospects but would also hold back FDI. Heightened volatility in international financial markets is another downside risk./.